30 May 2026

Mapping the Evolution of Token-Based Systems for Secure Recurring Transactions in Mobile Retail Environments

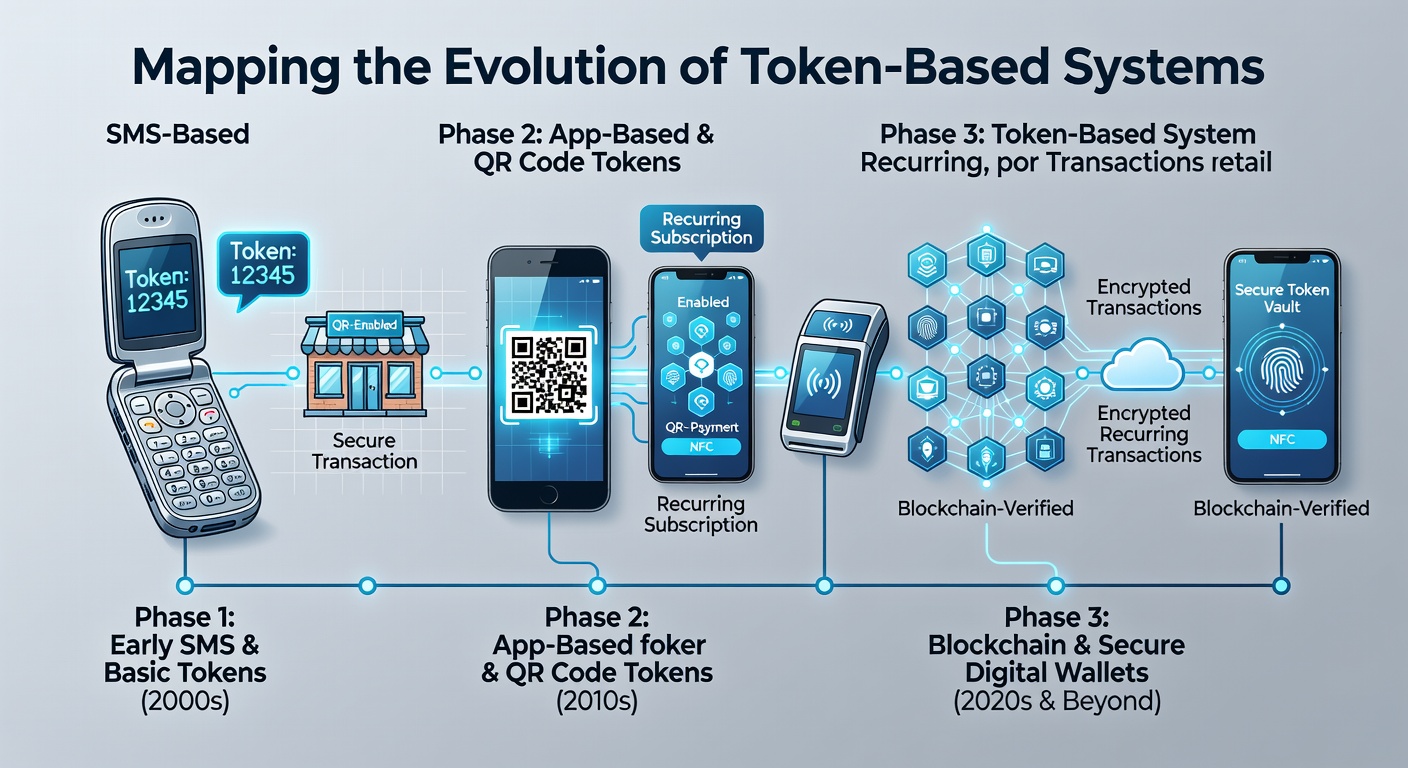

Token-based systems emerged as a response to growing security demands in digital payments, and they replaced static card details with dynamic, single-use identifiers that limit exposure during recurring billing cycles. Researchers trace the initial concepts back to the early 2000s when financial institutions began experimenting with temporary credentials to protect card-not-present transactions, while mobile retail environments accelerated adoption as smartphone penetration reached critical mass across urban centers worldwide.

By the mid-2010s standards organizations had formalized tokenization frameworks that allowed merchants to store references instead of actual payment credentials, and this shift reduced breach impacts because compromised tokens held no reusable value. Observers note that recurring transactions in subscription models benefited directly since each billing event could draw from refreshed tokens without repeated transmission of sensitive data, and mobile apps integrated these processes through background authentication layers that operated seamlessly for users.

Key Milestones in System Development

Early implementations focused on e-commerce checkout flows where tokens replaced credit card numbers in merchant databases, yet mobile retail introduced additional variables such as device binding and location-aware validation. Data from the Federal Reserve indicates that token usage in recurring mobile payments grew steadily through 2023 as platforms standardized application programming interfaces for token requests and lifecycle management. And in regions like Australia the Payments System Board documented similar patterns where contactless recurring deductions relied on tokenized credentials to maintain compliance with security mandates.

Subsequent phases incorporated multi-factor elements into token generation, and systems began linking tokens to biometric signals or behavioral patterns collected during mobile sessions. Experts at academic institutions including MIT documented how these enhancements addressed vulnerabilities in subscription renewals, since tokens could expire or rotate automatically based on predefined risk thresholds. Mobile retail environments saw particular gains because apps could initiate token refreshes without interrupting user experiences during periodic charges for services like streaming or delivery memberships.

Security Mechanisms and Technical Frameworks

Modern token-based architectures employ encryption at multiple stages, and they separate the token service provider from the payment processor to create isolation between data stores. Each recurring transaction pulls a fresh token mapped to the original account details only within secure vaults, while mobile devices handle cryptographic operations locally through hardware security modules. Research from European Central Bank publications highlights that such compartmentalization lowered fraud rates in recurring mobile billing by restricting the attack surface available to interceptors.

Token lifecycle controls include provisioning, activation, suspension, and deletion routines that merchants trigger via standardized protocols, and these controls prove essential in mobile retail where users frequently update payment methods or cancel subscriptions. Observers point out that integration with device-specific identifiers further strengthens recurring transaction security because tokens lose validity if moved to unauthorized hardware. In May 2026 reports from Payments Canada noted expanded testing of these controls across retail platforms, showing measurable reductions in unauthorized deduction attempts when tokens incorporated dynamic binding elements.

Network-level validations add another layer, and token requests undergo real-time checks against issuer rules before authorization proceeds. This process supports high-volume subscription environments where thousands of periodic charges occur daily, and mobile retail benefits because latency remains low while security protocols run in parallel. Industry analyses from the PCI Security Standards Council describe how token vaults maintain audit trails that allow retrospective review of recurring transaction sequences without exposing underlying account data.

Applications Across Mobile Retail Platforms

Subscription services in retail apps adopted token systems early because they required reliable periodic deductions without storing card details on user devices. Grocery delivery platforms and streaming services integrated token gateways that handled renewals through background processes, and these setups allowed users to manage multiple subscriptions from a single mobile interface. Figures from academic studies reveal that token rotation schedules aligned with billing cycles helped maintain continuity while limiting exposure windows during each transaction.

Peer-to-peer elements sometimes appear in hybrid models where retailers facilitate recurring payments between consumers and service providers, yet the core token framework stays consistent. Observers note that emerging markets saw accelerated deployment as mobile-first retail ecosystems bypassed legacy card infrastructure entirely, and token standards enabled cross-border recurring charges with localized compliance adjustments. What's interesting is how device manufacturers embedded token support into operating systems, which simplified developer access and encouraged broader adoption in retail applications.

Current Landscape and 2026 Developments

By May 2026 token-based recurring systems had incorporated elements of distributed validation in select pilot programs, and these tested resilience against centralized points of failure. Retail platforms reported smoother handling of subscription upgrades or downgrades because token references could update without full re-provisioning. Data indicates that interoperability between different mobile operating systems improved, allowing users to carry tokenized recurring arrangements across device changes with minimal friction.

Regulatory updates in various jurisdictions emphasized consumer control over token permissions, and frameworks required clear disclosure of how recurring charges linked back to original payment sources. Mobile retail environments adapted by providing in-app dashboards that displayed active tokens and their associated merchants, and this transparency supported user trust during periodic billing events. Research indicates continued refinement of risk-scoring algorithms that adjust token strength based on transaction history and device context.

Conclusion

The progression of token-based systems reflects ongoing adaptation to security challenges in recurring mobile retail transactions, and mapping these changes shows consistent emphasis on data isolation and lifecycle management. Technical standards evolved to support seamless integration across devices and regions, while validation mechanisms reduced opportunities for unauthorized access. Continued monitoring of deployment patterns in 2026 and beyond will document how these frameworks respond to new retail models and regulatory expectations.